Why Ontario Insurance Companies Reject Knob and Tube

Insurer fire-risk reasoning, common Ontario carrier policies, the 'uninsurable' pain point, and ESA Certificate of Acceptance as proof of remediation.

By Michael Chen, Licensed Master Electrician ·

Homeowner facing insurance non-renewal due to K&T needs to understand why and what fixes it.

Why Ontario Insurance Companies Reject Knob and Tube

Homeowners searching for solutions regarding insurance knob and tube ontario policies often call us in a panic after receiving a non-renewal notice.

We know exactly how stressful this sudden roadblock feels for local residents.

The reality is that carriers like TD Insurance might offer a short 30-day grace period, but a full electrical replacement is eventually required.

We are going to break down the exact reasons providers deny coverage and walk through the proper way to resolve the issue with the Electrical Safety Authority.

What This Guide Covers Regarding Insurance Knob and Tube Ontario

This overview outlines the exact steps required to reverse a situation where a carrier issues a k&t uninsurable ontario classification.

We built this resource to explain the specific roadblocks you face and the necessary upgrades needed to secure an ESA Certificate of Acceptance.

Understanding these strict requirements will help you avoid costly mistakes during the replacement process.

1. What Is the Insurer Fire-Risk Reasoning?

Century-old properties often rely on original 1920s wiring that struggles to safely power modern, high-draw appliances.

We find that the exposed live wires drastically increase the risk of an electrical fire when the rubberized cloth insulation flakes off over the decades.

Another major problem is that these circuits lack a dedicated ground wire to safely divert sudden power surges.

We constantly remind clients that a system originally designed for a few incandescent lightbulbs cannot handle today’s air conditioners or microwaves without severe overheating.

The Electrical Safety Authority of Ontario warns about several specific hazards flagged by underwriters:

- Degraded Insulation: The antique rubber and cloth wrapping simply crumbles away inside the walls.

- Lack of Grounding: Two-prong setups cannot manage power surges from modern electronics or appliances.

- Overloaded Circuits: The original 15-amp lines overheat quickly when running modern kitchens.

- Amateur Modifications: Decades of quick fixes often leave unsafe, hidden splices resting against dry wood.

2. What Are Common Ontario Insurer Policies?

Most mainstream carriers in the province will outright refuse to issue a new policy if an inspection reveals active legacy circuits.

We regularly deal with situations where buyers are left scrambling because their bank requires standard coverage to finalize the mortgage.

Some specialty providers might offer a temporary policy, but they usually charge exorbitant premiums to offset the risk.

We typically see carriers grant a strict 30-day to 60-day grace period to complete a full property rewiring.

A Licensed Electrical Contractor must then verify the upgrades to maintain the active coverage.

We prepared a quick breakdown of how different companies generally handle these outdated systems:

| Policy Type | Typical Carrier Response | Expected Timeframe |

|---|---|---|

| Standard Renewals | Immediate denial or non-renewal notice if discovered during an appraisal. | Zero days (Coverage dropped). |

| Specialty Coverage | Approved with high premiums and mandatory upgrade conditions attached. | 30 to 60 days to replace. |

| Post-Remediation | Standard rates restored upon submission of an official inspection document. | Immediate upon certificate delivery. |

3. What Does the ‘Uninsurable’ Pain Point Actually Mean?

A designation of uninsurable means standard companies view the property as too risky to cover, effectively blocking your ability to secure a traditional bank mortgage.

We watch many home sales collapse simply because the buyer cannot get the financing approved without standard property coverage.

This specific pain point translates directly into a massive financial headache for sellers who refuse to upgrade the system before listing.

We usually estimate a full residential replacement in Toronto costs between $15,000 and $25,000 depending on the property layout and size.

Removing this structural hurdle is the only reliable way to restore the property’s true market value.

We often explain the compounding financial costs of avoiding this critical remediation work:

- Lost Home Sales: Buyers walk away immediately when their lender denies the mortgage application.

- Expensive Premiums: Boutique insurance policies cost significantly more than standard monthly rates.

- Devalued Property: Buyers will heavily discount their initial offers to account for the impending $20,000 rewiring job.

- Safety Liability: You carry the absolute total financial burden if a fire starts from the original 1920s circuits.

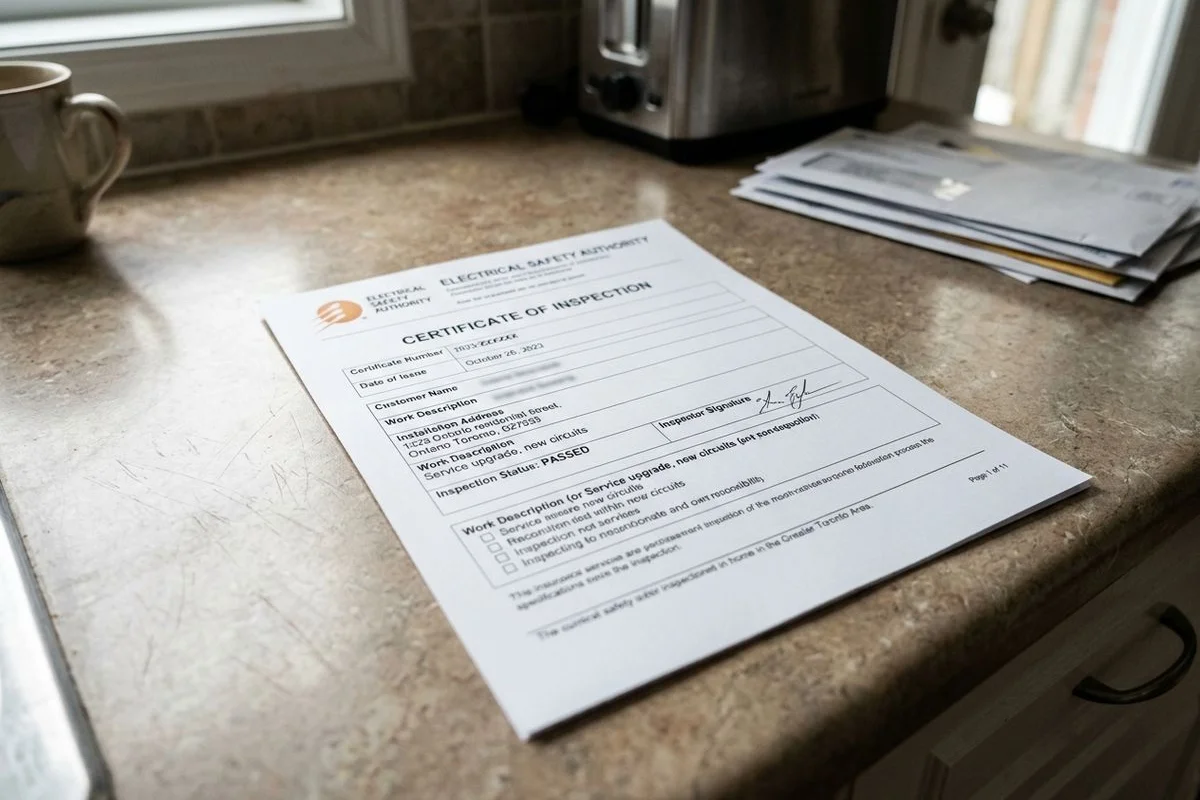

4. How Does an ESA Certificate of Acceptance Act as Proof of Remediation?

The ESA Certificate of Acceptance is the legally recognized document proving your home meets the strict safety standards of the current Ontario Electrical Safety Code.

We always pull the necessary permits in our specific LEC name, because homeowner-pulled permits transfer all the liability directly to you.

This critical piece of paper serves as the exact k&t insurance proof your broker needs to see to reinstate standard coverage immediately.

We bake the permit and inspection fees directly into our flat-rate quote so you never see a separate, unexpected line item.

A final review by an official ESA inspector guarantees the hazardous materials are completely isolated.

We handle this entire strict compliance process directly for our residential clients:

- Initial Assessment: An electrician identifies all active century-old circuits hiding behind the walls.

- Permit Registration: The contractor files the official notification with the Electrical Safety Authority.

- Complete Replacement: All outdated components are completely removed and replaced with modern, grounded wires.

- Official Inspection: An ESA inspector carefully reviews both the rough-in and final finishes.

- Certificate Issuance: You receive the official document to forward straight to your designated underwriter.

5. What Does a Sample Insurer Letter and Our Written Response Look Like?

A typical warning letter will clearly state that property coverage will be terminated on a specific date unless the outdated wiring is completely eradicated.

We respond to these strict demands by providing a comprehensive remediation plan printed directly on our official company letterhead.

This detailed document explains the scope of work, provides our ECRA/ESA license number, and establishes a firm timeline for the project.

We find that underwriters are much more cooperative when they see a professional, structured plan from a verifiable Toronto contractor.

Your insurance broker can often use this official documentation to successfully negotiate a short extension while the repairs take place.

We include several mandatory pieces of information in our standard response to carriers:

- Contractor Credentials: Our official ECRA/ESA license number proving our legal standing in the province.

- Permit Details: The specific, traceable ESA notification number assigned directly to your property.

- Scope Summary: A clear, written statement that all visible legacy lines will be safely disconnected and replaced.

- Completion Date: A firm, documented schedule showing exactly when the final Certificate of Acceptance will be available.

Ready for a Quote?

Securing standard property coverage requires definitive action and professional execution.

We are happy to provide a free estimate on residential projects across the Greater Toronto Area to help you meet your insurance knob and tube ontario requirements.

Every complete rewiring job ensures that the necessary legal permits are registered correctly under our official LEC name.

We guarantee that your final Certificate of Acceptance is always included to satisfy your underwriter completely.

Visit our knob and tube wiring replacement page to review the full scope of our services, or simply contact us directly to get started.

For more context on related decisions, read our guide on how to Identify Knob and Tube in Your Toronto Home.

Frequently Asked Questions

Will any insurer cover active K&T?

+

A small number of specialty insurers will, typically with high premium and inspection requirements. For Toronto homes specifically, we handle this through our LEC with the ESA permit included in the flat-rate quote. Free estimates on residential projects.

Does abandoned K&T count?

+

Usually no. Insurers generally accept abandoned (de-energized) K&T if it's been confirmed disconnected. For Toronto homes specifically, we handle this through our LEC with the ESA permit included in the flat-rate quote. Free estimates on residential projects.

Will partial replacement satisfy the insurer?

+

Most insurers want full active-K&T removal, not partial. For Toronto homes specifically, we handle this through our LEC with the ESA permit included in the flat-rate quote. Free estimates on residential projects.